News

Future Energy Consumption and Planning

When you think of what’s going on in the world, you’d think that we were living in a dystopian future conjured out of the imagination of Aldous Huxley, Margaret Atwood or Ray Bradbury.

We have a global pandemic that has infected 474 million, accounted for 6.1m lives and devastated global travel, migration and labour markets. A war is raging in Europe, destabilising nations, creating fear, destroying lives, and straining global relationships to breaking point. Record low-interest rates are rapidly disappearing as inflation takes hold driven by increased costs of goods, materials and supply. Seemingly successful businesses like ProBuild and CONDEV are failing due to huge material price increases that cannot be passed on to clients or end-users. Fuel prices are at an 8 year high in Australia and the same pain is being felt by consumers of steel, aluminium and other critical resources.

It is a perfect storm, that I am sure will inspire the next generation of dystopian fiction writers, but, until we can get lost in a good book, the reality for many is that we must tighten our belts or look for alternative solutions that can reduce the cost of doing business and cost of living pain.

The challenge for us in Australia is how we do so, given that we are a fairly small market, a long way from most major markets? This means that despite our relative global wealth, we are often at the back of the queue for new technologies for supply and competitive pricing. And what does it mean for the construction and infrastructure sector?

When we looked at concepts for Construction in 2050, we looked at how a quick gain for the sector and society can be earned through electric and hybrid vehicles. But that’s not without challenges:

- While many car manufacturers have committed to electric-only vehicles by 2030, they are faced with challenges:

- The cheapest EV in Australia is the MG ZS EV which can be driven away from $46,990 meaning it is out of reach for many Australians, given the average drive away price of a new (non-electric) vehicle is $40,729 according to Canstar so price is a factor.

- Supply is also an issue, with many manufacturers not bringing their key models to Australia. Ford UK offers hybrid versions of its core models, Ford Australia has a much more limited range for comparison. With short supply and limited availability, price parity is not expected for around 5 years. It also means long wait times for purchasers, with accounts of a dealer selling 11 EV cars last weekend when they normally sell two but can’t deliver to customers until 2023.

Possible Solutions

The biggest barriers to consumer and fleet uptake of EVs in Australia are:

- Price

- Charging infrastructure and vehicle range

- Supply

The Queensland Government has announced a rebate program for EV purchase, returning $3,000 to purchasers of new vehicles under $58,000. A positive move, but perhaps one that will not garner huge change given the pricing and spend figures mentioned earlier. In the same announcement, further investment was also released to support increased charging infrastructure, particularly investment in regional stations.

It is essential for steps to be made to increase charging infrastructure as that negates the range barrier and will enable Australians to have confidence that their EV will get them to where they need to go…and back again. This will in turn drive demand and may see more affordable models from more manufacturers enter the market.

Some other areas that could be considered:

- Investment in-home charging points – Could a scheme be implemented, similar to the solar rebate that enables homeowners to add charging points with grants from government? In addition, similar grants could be made for carparks, residential body corporates, and commercial property managers to retrofit charging stations into established buildings.

- Funding retrofit programs – It is possible to retrofit electric motors into existing cars, but it is extremely expensive and highly regulated – as it should be – but investment in such technology would see the price come down and make it easier for people who don’t want or can’t afford a new vehicle to make a positive change.

- Business premises and residence planning regulations – New developments could be mandated to include charging point infrastructure as part of their planning approvals. In the same way that there is a ratio of carparks to units, perhaps charging points could become a future metric?

In addition to those measures, it is good to see investment being made in rare earth metals, those elements on the periodic table that are essential to battery technology. A $243m funding announcement for critical minerals processing is a great start as it will enable Australia to take advantage of natural resources critical to future manufacturing.

What Does This Mean for Construction?

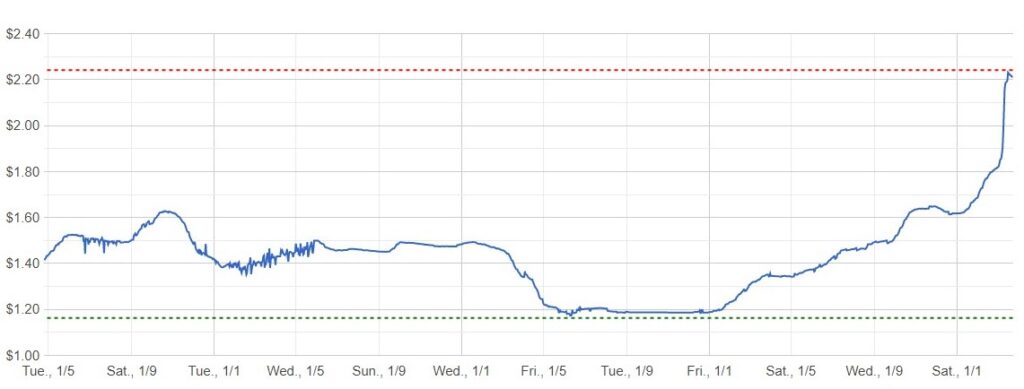

The construction sector is as challenged as consumers by the fluctuating cost of resources, and is vulnerable to price swings. For example, on a project, you may have a fleet of large dozers, each consuming around 500 litres per day of diesel. When pricing and winning the work, 2 years ago, your costs were factored in based on appropriate resources costs, calculated inflation and a normal series of risks that correctly didn’t involve a global pandemic, a major conflict and escalating fuel prices.

Graph via Monitoring of Diesel Prices in Queensland

Therefore, a project’s margins – often already wafer thin – are under more pressure due to an essential commodity increasing in cost way above an average forecast. This becomes particularly stark when we look at everything, we utilise on a project that is powered by diesel or diesel generators. Factor in major prices changes to steel, aluminium, timber and more and a profit squeeze is taking place.

We are also faced with the challenge that we do not have workable alternatives for plant, equipment and our fleet of utes and site vehicles. Neither does our supply chain. There are a few electric mini excavators on the market such as the JCB 19c-E and while welcome additions, they cannot meet the needs of a large-scale project. Presumably, for larger vehicles, the battery scale, torque and power, range, and charge requirements are not possible given the currently available technology.

Potential Solutions

Firstly, we may well need to consider how we price and allocate resource price risk within a project – at least in the short to medium turn to enable multi-year projects to take into account a more wildly fluctuating resource market. This could also be reflected in contracts that enable cost recovery if prices fluctuate beyond an agreed set of variations.

In addition to how we price projects, we need to:

- Push for greater consumer investment and roll-out of EVs – When manufacturers realise the benefits of scale and pricing that comes through greater consumer adoption, technology will improve allowing for more efficient and powerful batteries. This, in turn, will benefit the requirement of the construction sector for fleets of utes, trucks, machinery and more.

- Create and secure a supply chain for future EVs – A complete approach needs to be taken to secure the resources and technologies required to produce batteries and create a vertically integrated supply chain with local supply and manufacture.

- Invest in infrastructure required to support EV roll-out. From green and renewable energy sources (wind, solar, pumped hydro) on macro and micro scales to residential and commercial fast charging points, infrastructure gives confidence that power is available when required.

- Create infrastructure and industry to repurpose and recycle precious materials to create a disposal strategy for batteries that are no longer usable.

- Don’t put all our eggs in one basket – Based on what we learned from the LPG vehicle experience, a single option moving forward is not the answer. With a rapidly growing hydrogen sector, hydrogen-powered cars are available and Toyota is trialling three vehicles in Australia with 5kg of compressed hydrogen enabling 550km of cruising. The only challenge – there is one refuelling point in Australia and it is owned by Hyundai.

Environmentally, commercially, and socially, our industry needs to transition to a decarbonised future. But to do so, we need infrastructure that is stable, reliable, accessible and affordable. At CPP we are firm believers in this, but we fully understand that while the electric future is almost in our grasp, there is still a way to go, and unfortunately some shocks to bear on the way.